On January 3, the US launched an attack on the Bolivarian Republic of Venezuela and kidnapped President Nicolás Maduro. While the legal assessment appears largely undisputed (see here, here, here; denying an armed attack, Safferling), the analysis of the factual background lacks clarity. US President Donald Trump publicly claimed that the invasion of Venezuela took place inter alia because of oil and other resources. This ends the US approach of pursuing economic interests under the guise of promoting democracy. Given the blatant lies of the past, this unusual candor of US officials could in principle be appreciated, but it must be questioned. This blog post argues that oil and resources only indirectly guided the invasion, and that a comprehensive understanding requires an analysis based on geoeconomics and its consequences for global peace. The invasion has to do with the US dollar and the US’ fundamental debt problem—which seem to create an ever-stronger necessity for violating global peace.

After clarifying why blaming oil is unconvincing, the post concludes with a call to engage more intensively with the oft-ignored monetary and financial foundations underlying armed conflicts. It will try to offer an alternative approach to the reasonable, yet unproductive reaction of most international lawyers which (once again) proclaim or prophesize the erosion of international law.

The Long 20th Century of Oil Interventions

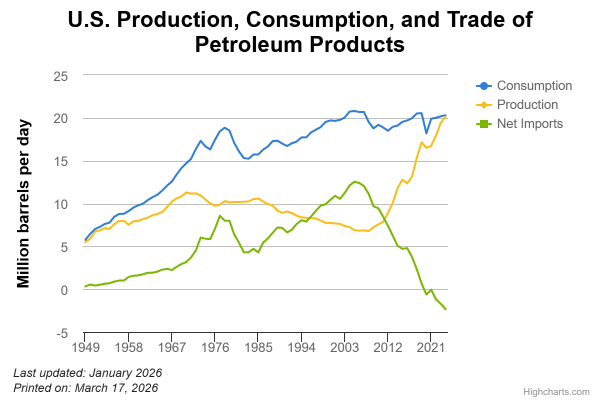

Most US interventions during the 20th century have been a key instrument to secure energy for domestic use since the US did not produce as much oil as it needed (Painter, pp. 29 et seq.). The 1953 CIA-backed regime change in Iran (CIA report, pp. 40 et seqq.) ended the reign of Mohammad Mossadegh, former prime minister of Iran and responsible for the nationalization of the Iranian oil industry (then mainly the British oil industry). This pattern continued with US involvement in the Second Gulf War and the invasion of Iraq in 2003, illustrating how America’s oil needs often led to military engagements. But the economic landscape has changed profoundly since then. US domestic production of crude oil has almost tripled compared to the early 2000s, making the US the largest oil producer globally, ahead of Saudi Arabia (and more than Russia and China combined). With consumption remaining constant, this has greatly contributed to the US becoming almost independent from oil imports (see chart).

However, this does not rule out the option of invading Venezuela in order to sell the oil abroad and thus profit in another way. While this has already happened, the expected profit is not substantial enough to justify an armed attack—which also explains oil companies’ apparent reluctance to invest in Venezuela. At less than US$60 per barrel, the oil price is experiencing its lowest point since the pandemic. This indicates market saturation, meaning that producing more oil would only decrease the value further. Assuming the US administration has a basic grasp of economic theory, there is little reason to believe that the invasion of Venezuela was only because of oil. Instead, we must engage with the US debt problem to understand the underlying reason for this and many other contemporary conflicts.

U.S. Energy Information Administration (2026).

38 Trillion

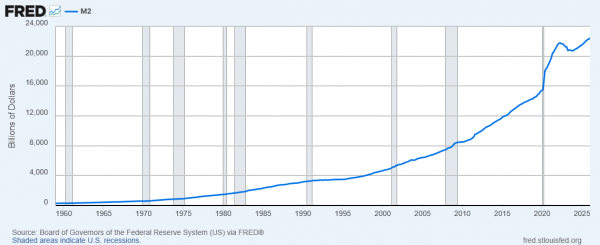

US$ 38,564,513,699,490.46. This is the exact amount of US debt as of February 4, 2026. Most people (including the author) will have trouble saying this number out loud, let alone imagining it. And that is precisely the point: nobody assumes that the US will ever effectively refinance its total debt. Instead of paying its debts down to zero, the US Treasury takes on new debts to pay off old ones (roll over). The sheer amount of its debt only matters to a certain extent. It is much more important that the US remain solvent and pay interest which is guaranteed by a vital economy and high tax income. To preserve the competitiveness of the US economy, in turn, the Federal Reserve Bank (FED) tries to keep key interest rates low and purchases assets and government bonds from private banks with newly created USD (Quantitative Easing). This enables banks to give out loans at low interest rates which supports the private economy. By doing this, the FED steadily extends the money supply (see chart) which—under normal circumstances—would lead to high inflation. That is what we have seen, for instance, in the case of Argentina in 1989, whose Central Bank created additional money leading to hyperinflation (Beckermann, p. 667) with devastating social consequences. The US’ extension of money supply, however, does not usually lead to considerable high inflation. And that is where the oil comes into play.

Board of Governors of the Federal Reserve System (US) via FRED (2026).

The Mythical Petrodollar

From basic economic theory, we know that the extension of supply only leads to lower prices (for currencies, this is inflation) if demand remains equal. If demand increases proportionally, prices remain stable. Since the USD is the global reserve currency (58% of all state reserves are US dollars) demand for the USD is guaranteed. But states do not hold their reserves in US currency for charity, nor by chance. They do it because the USD is the most useful currency. The usefulness of a currency is measured by the ability to trade goods with it. The Iranian Rial, for instance, is almost useless because Iran is subject to a severe global sanction regime. In contrast, the USD is universally recognized and—most importantly—used to trade basic resources, in particular petroleum. In 1974, when Saudia Arabia agreed on selling its oil almost exclusively in US dollars, the term Petrodollar evolved (for the history of the Petrodollar, see here). Other states holding reserves in US dollars guarantees steady and even rising demand. This introduction to geoeconomics is necessary to demonstrate the fundamental relevance of the Petrodollar for the United States. Abolishing the Petrodollar and replacing it with another currency would lead to decreasing demand followed by high inflation, and eventually to a high probability of US bankruptcy.

Invading Venezuela sought to prevent this precise scenario: in 2017, Maduro announced that Venezuela would turn away from the USD and sell its oil in other currencies (mainly the Chinese Yuan). Venezuela is the country with the largest—19% of global—oil reserves. However, due to kleptocracy, economic inefficiency and global sanctions, Venezuela provided less than 3% of global oil supply, rendering Maduro’s decision rather irrelevant to the Petrodollar’s strength. Nevertheless, the prospect of the world’s largest oil reserves being traded in Yuan was untenable for the US in the long run. Venezuela put on the pressure by asking to join BRICS in 2023, increasing the likelihood of closer cooperation with China. Though Brazil vetoed Venezuela’s admission because of personal differences between Presidents Lula and Maduro, a change of government following Brazil’s elections this year could clear the way.

Even back in August 2017, Trump attacked Venezuela verbally, stating that he was “not going to rule out a military option”. While the reasons for the exact timing of this operation are confidential, the foundation—at least largely—is sovereign debt-related.

The Need for Geoeconomic Peace Research

Recognizing that the attack on Venezuela was (partially) aimed at dollar stabilization highlights the monetary and geoeconomic logic of US foreign policy. It is more than understandable – and arguably compelling – that a President seeks to prevent national bankruptcy. But the US has got itself into a position in which national bankruptcy can arguably only be prevented by influencing other state’s oil policy. And if that cannot be achieved through negotiations nor through sanctions, military action emerges as the ultima ratio. This leads us to a fundamental question of international law: is the debt-based financial order, including the dollar hegemony, able to maintain peace? If not, what are the consequences?

Approaching this question requires (international) law scholars to leave their comfort zone and engage with numbers, empiricism, and finances. With global sovereign debt constantly rising since the financial crisis (and accelerated by the pandemic), peace-related consequences of debts may only be starting to show. The International Monetary Fund expects the world to hit the global debt rate of 100% by 2030. That would mean the world’s debt equals the world’s GDP, i.e., its value. This unprecedented event would bring uncertainty for the stability of the system, financially as well as politically. If the international law of peace wants to be more than an academic utopia and make a real difference, it must understand the geoeconomic dynamic of debts, and how it might influence global peace.

Even though there are some scientific works on the interconnection between finances and armed conflicts (e.g., here, here and to some extent here) the discourse lacks structural assessment and general backing in academia. To conclude that there are logical (at least in an economic sense) reasons for starting armed conflicts is often interpreted as justifying the use of force rather than as a critique of a system that sets economic incentives for wars. This needs to change.

Conclusion and Outlook

The Venezuelan case illustrates that wars are no longer fought primarily for territorial expansion or ideological dominance, but for the preservation of monetary and financial stability. Thus, the question for international law is not only how to prevent states from resorting to force, but how to reshape the global financial system so that peace is not structurally dependent on debt, currency hegemony, and the control of natural resources. True peace will require moving beyond moral condemnation, toward an understanding of the material foundations of power—and their legal reflection. Only by integrating monetary aspects into peace research, international law can hope to reclaim its relevance in an era where global debt is one of the biggest threats to global peace.

The “Bofaxe” series appears as part of a collaboration between the IFHV and Völkerrechtsblog.

Joel S. Bella is a Research Associate and PhD Student at the Institute for International Law of Peace and Armed Conflict in Bochum.